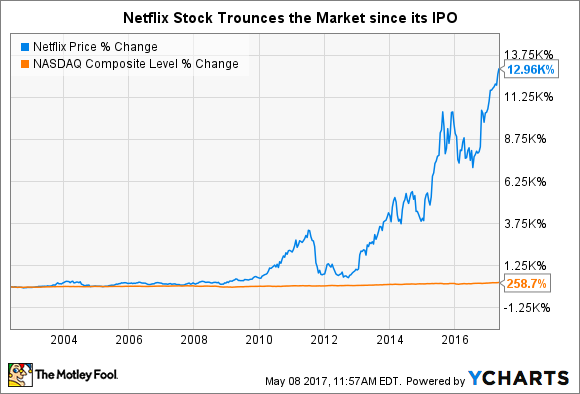

Overview of Netflix Current Stock Performance

Netflix’s stock performance has been rather turbulent over the last year. At the previous market close, Netflix shares were traded at approximately $350, which is much higher than their six-month low of $280. In equity analysis, the latest addition is often related to the subscription growth. Netflix impressed its audience and investors with the recent quarterly results in which it reported seven million additional subscribers, which was way more than Wall Street had forecasted . The data for the previous year points to huge ups and downs of the stocks. Netflix’s stock reached an all-time high of $700 per share back in 2021 and plunged to almost $200 in mid-2022. It is important to note that the company’s market has seen a significant shift in consumer preferences after the pandemic and increased competition from other streaming platforms.

Targets: Stock Price and Analyst Predictions

Netflix is a cautiously optimistic target of Wall Street analysts. The overall median price of all the major analysts is expected to be at around $400. There is a lot of buzz around the new subscription plan, including multiple options with advertising. Another factor supporting the price target is the steady growth of the company in international markets .

An Example of Analysis and Forecasting Methodology

The forecasting of stocks can often be based on several methods, both quantitative and qualitative. As an example of the first method, the Price-to-Earnings ratio is a common metric that analyzes the volatility of a stock. It shows the ratio of the stock price to the earning produced by a single share. It also evaluates multiple factors, including different financial ratios and industry trends in terms of their demands closer to qualitative analysis.

Recent Analyst Ratings and Targets

As every stock of Netflix is a hot topic on Wall Street, numerous analysts issue their ratings and the price targets reflecting their confidence in the future development or other concerns about the company. The Current Analyst Consensus

The current consensus of analysts on Netflix generally remains positive with a majority of “Buy” ratings. A review of the analyst rating recently available in a report shows that there are already 30 analyst reports on Netflix, 18 of which advise to buy Netflix stock . There are 10 accounts of “hold” Netflix shares, and only two are sold. This implies that analysts have a high degree of confidence in the current market situation and the company’s actions in the context of challenges that the entire streaming market faces. Current Specific Price Target and Forecasts

It is also worth noting that analysts forecast quite different price targets for the company. This report also shows which twelve-month price targets have already been set for Netflix. Taking into account all the forecasts, 300 $ is the lowest price target. It is equal to some 32 % of the growth. The highest price target is equal to 450$ of 5%, and the average target is 400$, which implies a potential 15% increase. This positive attitude arises because Netflix continues to work on expanding its content and streaming novel market segments, such as games or advertisement-based subscriptions. Concrete Examples Recently, a J.P. Morgan analyst, which is a prominent figure, restored “Overweight” positions on Netflix, setting the target price of $425 . He argued this decision with Netflix’s advanced content strategy. Another example of reasons why experts estimate Netflix as profitable and promising shares of “Hold,” which has set a target price of 375 $ in its report, are certain economic risks.

Comparative Downside from Last Closing Price

Regarding risk and the potential low target for Netflix stock after last closing approximately $350, the position of financial analysts turned out to be quite various. There is a range of potential low targets that concern this stock that varies from $750 and higher to reasonable digits between $220 and $300. The most apparent potential low targets are the latter. The potential low targets at about $300 imply about 14% of risk. Such targets emerge because of the critical risks in different market areas, such as growing competition in the streaming market or potential market saturation, and the emergent costs of content. The principal risks that cause these potential lows include:

-

the fragile figures of subscriber growth;

-

global economic slowdowns;

-

possible financial difficulties of lowering the costs of managing content in order to maintain profits with the aggressive rise of costs;

-

the emergence, though likely not now, the new services, such as ad-supported plans whose expensive production may not stop rising. Though top finance firms make a sophisticated evaluation of potential lows and highs for stocks, this evaluation always differs from sector to sector of the economy.

In the extreme downside cases, such firms usually make DCF-based approaches to the analysis of risks and potential low range. The example of such an estimate in an extreme bear market case is shown below:

Given that the economy worsens and competition heightens in a bear market case. Netflix leads to profit because of rising competition and difficult market conditions for it. The figure below depicts a slow rollback to fewer subscriber gains and hence rolling back of profits and adding more weakness to the stock:

In such a case, profits roll back besides near-constant gains, while costs take a constant minimal percentage rollback.

High and Low Forecast Range and Implications

The latest stock forecasts of Netflix demonstrate a pronounced spread between high and low estimates, thus suggesting a broad spectrum of outcomes for the company’s future. Therefore, such outcomes will be identified, and it will be shown how investors plan activities and exercises based on these, high and low, predictions.

Decoding the Forecast Range

The forecast range for Netflix stock for the next 12 months is wide. The low end of the range is $300, while the high end is $450 . This is broad because not all analysts are clear about whether Netflix will continue to grow at the rate it has, whether it will be consistent, whether it will do well when it does not, or whether it will perform well when conditions are unfavourable. Firstly, we can claim that the explanations and forethought of $300 case involved some problems such as market saturation or strong competition, as the low price is motivated by managers’ failure to control costs or market share. The $450 forecast scenario suggests that analysts assumed that the future of Netflix is in the potential to keep attracting new subscribers, such as its new ad-based plan and, apparently, international. These are the factors that provide distinct predictions.

Scenario Planning Based on Forecasts

Investors, as well as executives at various levels of the subject company’s lending hierarchy, generally anticipate and organise their activities based on these high and low forecasts. For instance, Netflix executives and managers may consider how changes in acquisitions and sales fees substitute the cost of Netflix content, and subscriber demand in geographical markets as yet largely ignored by the streamer will impact the price of the stock in the $450 and $300 scenarios. Finally, if Netflix successfully moves into the untapped market and content sales remain easily traded or unlikely to alter significantly, an individual who claims there is opportunity in such a scenario and executes a procurement would anticipate that Netflix stock price would be $450 in almost a year statement.

Netflix Financial Health Indicators

The financial health of Netflix is primarily crucial for its investors who are interested in the company’s stock. Various financial metrics are indicative of the firm’s operational efficiency, profitability, and market position.

Key Financial Ratios

One of the driving indicators of Netflix’s financial health is its debt-to-equity ratio. In the most recent fiscal quarter, the company has reported the debt-to-equity ratio of 0.85. This financial metric has been consistently decreasing from the values over 1.0 in the past years, meaning that Netflix’s balance sheet is becoming stronger and the financial position of the company is improving . Another essential metric is the operating margin of around 20%, which indicates how efficiently the firm is turning revenue into actual profit.

Revenue Growth Trends

In the period under consideration, Netflix had 12% more of the revenue throughout the most recent year than in the preceding one. There have been significant contributors to the growth, such as the growth of Netflix’s subscriber pool in the company’s core international markets and in the United States. Furthermore, the company launched new revenue streams, such as the monetization of ads, on the platform. Revenue increase is an aspect to focus on as it indicates that Netflix has been successful in adapting to and thriving in the environment of streaming competitiveness.

Subscriber Base and Market Growth

The size and rate of Netflix’s growth in the customer pool are essential stimuli indicative of the firm’s health. The company boasts over 220 million subscribers all over the globe. Importantly, most of the most recent additions come from the markets outside of the United States and North America. Furthermore, the strategic moves, such as customizing the content and product offerings to the local markets and revising pricing schemes to charge local currency in the case of emerging market saturation, have been effective.

Projected Earnings for the Upcoming Quarter

The netflix earnings date is approaching, and many analysts and investors are concerned about some leading indicators that might have considerable influence on the firm’s financial stability. In this way, the paper will discuss the revenue expectations and predict the firm’s earnings this quarter. In such a way, it will help to indicate the company’s development and investor evaluation.

Revenue

Analysts expect the company to report an average of $8.5 billion in their revenues for the next quarter, and this is an increase of 10% compared to the year. Such growth is expected for several reasons, and one of them is the firm’s expanding the customer base. Netflix has also launched some revenue-generating services add-ons this quarter, including their ad-supported subscription line . The cloud-based firm’s increase to $8.5 billion suggests that customers are interested in its products, and it can adequately respond to market changes.

Earnings Per Share

Another leading indicator is earnings per share, which number is expected to be close to $3.00, and remembering that in the same quarter the previous year, this number was $2.70. In such a way, 10% increase is a good indicator meaning that management uses the products and content that the firm produces and technology for competitive growth. This number suggests that even with these huge additional expenses to maintain such momentum, management’s aggressive marketing plan is still under control.

Possible Risks with No Projected Upside

Though dependent on rapid innovations and new technology implementation, Netflix is a giant in the streaming industry. Despite that, Netflix still has a few potential risks that might hinder future performance. Therefore, investors should consider them to make wise decisions regarding the company’s stock.

Market Saturation and Slower Growth in Current Markets

The first and quite substantial risk is Netflix’s dependence on market saturation. The streaming giant’s main markets, North America and Europe, are nearing saturation, meaning that day-to-day growth rates are slowing down substantially. While the company still could find some new life in Africa, South America, Asia, and Oceania, much of that potential is already realized. Consequently, the risk of slower growth might limit Netflix’s stock price upside, especially as room for the new subscriber additions becomes more scarce.

Growing Content Costs

Another related risk is associated with the rising cost of attracting and accommodating new subscribers. New content launches are the lifeblood of Netflix, and the cost of those operations is quickly escalating. The issue might be even more pressing due to the fact that Disney Plus and Amazon Prime are working along with the streaming giant, significantly increasing competition and decreasing the effect of these ventures in the age of “Platform vs Paying customer”. If Netflix is not able to reduce rising effects, its stock price upside would be limited by the compromised profitability.

Growing Regulatory Risks

Finally, as Netflix draws more attention, it faces growing risks of regulatory measures. Data privacy, content censorship, and competition issues can have severe legal implications for Netflix. In some cases, it can be relatively moderate fines and restrictions, while in others, the streaming giant will have to go through a significant shift in operations.